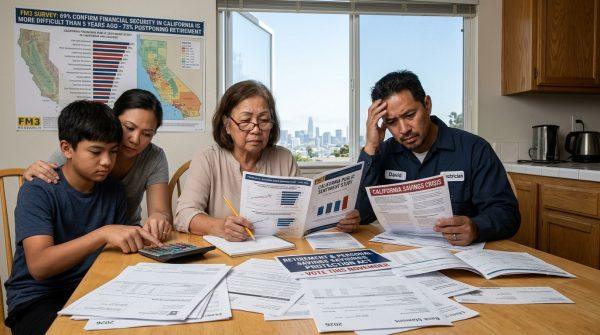

For many Californians, the dream of a comfortable retirement is slipping away. A recent survey by FM3 Research, conducted between April 15 and April 22, 2026, reveals that financial security is the top concern for voters across the state. The study, which polled 867 likely voters, paints a stark picture: 85% of respondents say high taxes and the rising cost of everyday essentials make it nearly impossible to build a solid retirement fund.

This isn't just about pinching pennies. The data shows that 69% of Californians believe the financial landscape is significantly tougher than it was five years ago. For many, this has created a constant state of anxiety, with a growing number considering leaving the state altogether to protect their long-term economic future. The crisis is particularly acute for Latino families, who often carry the dual burden of supporting both their immediate households and relatives back in México, Centroamérica, or other parts of the diaspora.

The Savings Crisis Hits Home

The ripple effects are profound. According to the survey, 73% of participants personally know someone who has had to delay retirement due to financial pressures. This isn't a niche problem—it's a widespread phenomenon forcing Californians to rethink their life plans. Many now estimate they need savings exceeding $1 million just to achieve basic stability, a daunting target in a state where the cost of living continues to climb.

Experts at the Hoover Institution have warned that any future legislative attempt to tax personal retirement accounts is a “real threat.” This perception has already changed behavior: 65% of voters now plan to work longer than they originally intended, hoping to avoid the direct impact of shifting government policies on their personal finances. The lack of predictability in state revenue strategies only deepens the collective anxiety, making long-term planning feel like a gamble.

A Legislative Lifeline: The Retirement & Personal Savings Protection Act

In response, a broad coalition of labor unions, veterans groups, and business organizations is championing the Retirement & Personal Savings Protection Act, which will appear on the ballot this November. The proposed law aims to prevent the state from imposing new taxes on retirement accounts, offering a clear line of defense for personal assets. Roughly 80% of voters already support legal frameworks that guarantee the security of private property and accumulated retirement funds.

Financial advisors across California are urging clients to seek savings schemes with greater predictability, given the volatile fiscal environment. Community organizations are also stepping up, monitoring legislative proposals to ensure the interests of older workers—especially those in Latino communities who often lack access to employer-sponsored retirement plans—are not overlooked.

The path toward stability, however, requires more than just a single ballot measure. As the November elections approach, economic security has become the central theme for voters. This moment is crucial for defining the safeguards that will protect family wealth, ensuring that retirement planning ceases to be a source of constant anxiety. For Latino families in California, who have built their lives through decades of hard work, the stakes couldn't be higher.

For more on how inflation and rising costs are squeezing Latino seniors across the US, read our report: Retirement in the US: How Inflation and Rising Costs Are Squeezing Latino Seniors. And if you're considering a move, check out our analysis of US Housing Market Correction: 8 Cities Where Prices Are Expected to Drop in 2026.